Recessions & Sharemarket Returns | what should investors expect?

The experience of an economy in recession is unfamiliar to many Australians, if not a fleeting memory for those that lived through the early 1990s.

As unfamiliar as recessions are, it would seem that the historical relationship between recession and share market returns are a complete unknown (oddity) to investors.

With the fear of the unknown being a very common theme at present, it is important to look to the experience of the past to provide key insights to what we might reasonably expect to transpire both during and in the period post a recession in both an Australian and global investment context.

Economists define a recession as two consecutive quarters of declining economic growth. In more common terms, a recession is characterised by a significant reduction in business activity, rising unemployment and declining business and consumer confidence.

Although yet to be officially confirmed, it is already widely accepted that Australia has now entered recession for the first time since 1990-91, bringing an end to a record breaking run of economic prosperity. This extraordinary circumstance may have continued for some time but for the economic lockdown imposed by Governments in an effort to contain a one in a hundred year event – the COVID-19 Pandemic.

It is important to note that whilst Australia’s robust economy avoided a technical recession during the fallout from the Global Financial Crisis (GFC) more than a decade ago, this was not the case for most other developed economies.

So investors in broadly diversified portfolios that include global shares have considerable historical information to draw upon during this and earlier periods to assist in determining what to expect.

The first and most important learning is that the sharemarket is not the economy.

This notion has profound consequences for investors. It means that what is happening in the real economy doesn’t necessarily correspond with the returns obtained by investors in the sharemarket, and this is particularly the case over shorter time periods.

The reasons for this need some explanation.

For example, in Australia the mining and financial services sectors represent approximately 20% and 27% respectively of the largest 200 ASX listed companies. In contrast, these same sectors account for only around 10% each of the overall Australian economy (GDP).

From an employment perspective the distinction is even more striking.

The two sectors account for nearly a quarter of jobs amongst the top 200 companies, but scarcely more than 5% of jobs in the broader economy.

To put this another way, the overwhelming majority of companies here and overseas are privately owned and have not sought to publicly raise capital on sharemarkets. As such, their shares are not available to be traded and their performance (both good and bad) doesn’t show up in the returns enjoyed by investors in public listed company shares traded on the Australian Stock Exchange and other global sharemarkets.

There can be little doubt that, notwithstanding the difficulties faced by larger companies, the viability of many smaller businesses is on a precipice as they are often not as well capitalised and don’t have access to the same resources, opportunities and funding as larger listed firms.

Another crucial point to note is that sharemarkets are forward looking.

That is, they tend to anticipate what might happen in the real economy, and of course this is always changing as new information becomes available, which then gets reflected in share prices.

Global research firm FTSE Russell analysed 30 recessions (including the Great Depression) in the US economy over a 150 year period from 1869 to 2018.

Amongst their key findings they observed the following;

- On average the US sharemarket peaked around 6 months before an economic recession commenced, (but it is important to note this did not always coincide with a recession and is only apparent with the benefit of hindsight);

- There was a very poor inverse correlation of -0.1 between US sharemarket returns and GDP changes across the 30 recessions that occurred during the study period (indicating that investor returns aren’t dependent upon the economy);

- Sharemarket returns were negative in only 14 of the 30 recessions studied (indicating that economic recession isn’t necessarily bad news for share investors) ;

- For investors to successfully profit from anticipating an oncoming recession and adjusting their investment holdings accordingly, they would have required an extraordinarily high 77% forecasting accuracy, which would need to be even higher after taxes and transaction costs are taken into account;

More broadly, research by the International Monetary Fund (IMF) identified 122 recessions in 21 developed economies in the period from 1960 through to the onset of the GFC in 2008. The IMF observed that recessions are usually relatively short and last about 12 months. It is also noteworthy that recessions have become shorter and less frequent over time as economies have matured and policy responses have become more targeted and better refined.

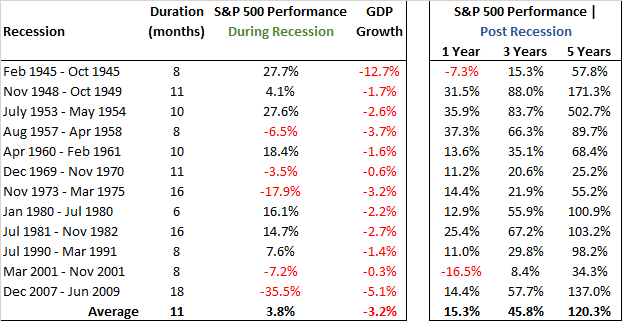

Whilst it is virtually impossible to predict exactly when a recession will begin and end, historical share market returns following recessionary periods have been significantly positive most of the time. The following table highlights the 1, 3, 5 year total returns following the end of US recessions over the past 75 years:

Of note, there was not a single 3 or 5 year period following a recession where shares declined and in 5 of the past 11 US recessions, the broad share market index rose by >100% over the ensuing 5 years.

Closer to home, Australia’s 1990-1991 recession lasted for around four quarters. During the calendar year of 1990 the S&P/ASX All Ordinaries Index fell -17.5%, however for the 12 months ending December 1991 the market grew +34.2% and over the 3 and 5 year period ending 1993 and 1995 grew by +83.2% and +101.7% overall.

Whilst this may seem counterintuitive at first, it should not be surprising for the reasons outlined above, and as indicated is by no means unusual.

Put simply, the premium for investing in shares should reasonably be expected to increase during periods of heightened economic uncertainty to compensate investors for elevated levels of risk.

Given the speed and severity at which the current global recession arose, only time will tell whether the economic recovery is equally swift, or is protracted because of recurrent outbreaks of the virus.

In either case, investors should remain focussed on the things they can control and not become overly distracted by unpredictable economic events which may have only minimal impact on long term investment outcomes.

Other issues to consider are the potential consequences of withdrawal and winding back of the monetary and fiscal stimulus measures that have been implemented by Governments and Central Banks over the past few months, along with the possible introduction of further protective measures to keep the global economy afloat.

Based on APW Partners observations from previous recessions in Australia and around the globe the best course of action for long term investors is to maintain a well-diversified portfolio of shares, property, bonds and cash, avoid the temptation to seek shelter from the economic storm when the rewards are often greatest, and have a predetermined plan that prevents becoming a distressed seller when prices are temporarily depressed.